Affiliate disclosure: This article contains affiliate links. If you click and purchase, we may earn a commission at no extra cost to you.

Table of Contents

◉ Introduction ◉ Reader Roadmap ◉ The Short Answer ◉ What a Business Entity Actually Does ◉ The Main Business Entity Options ◉ Entity Comparison ◉ How LegalZoom Fits ◉ The Practical Decision Framework ◉ Step-by-Step ◉ Practical Examples ◉ Cost and ROI Considerations ◉ When Not to Form an LLC Yet ◉ Common Mistakes and Troubleshooting ◉ LegalZoom vs. DIY vs. Hiring an Attorney ◉ Privacy, Compliance, and Data Considerations ◉ The Beginner’s Entity Selection Checklist ◉ FAQ ◉ Conclusion ◉ Sources

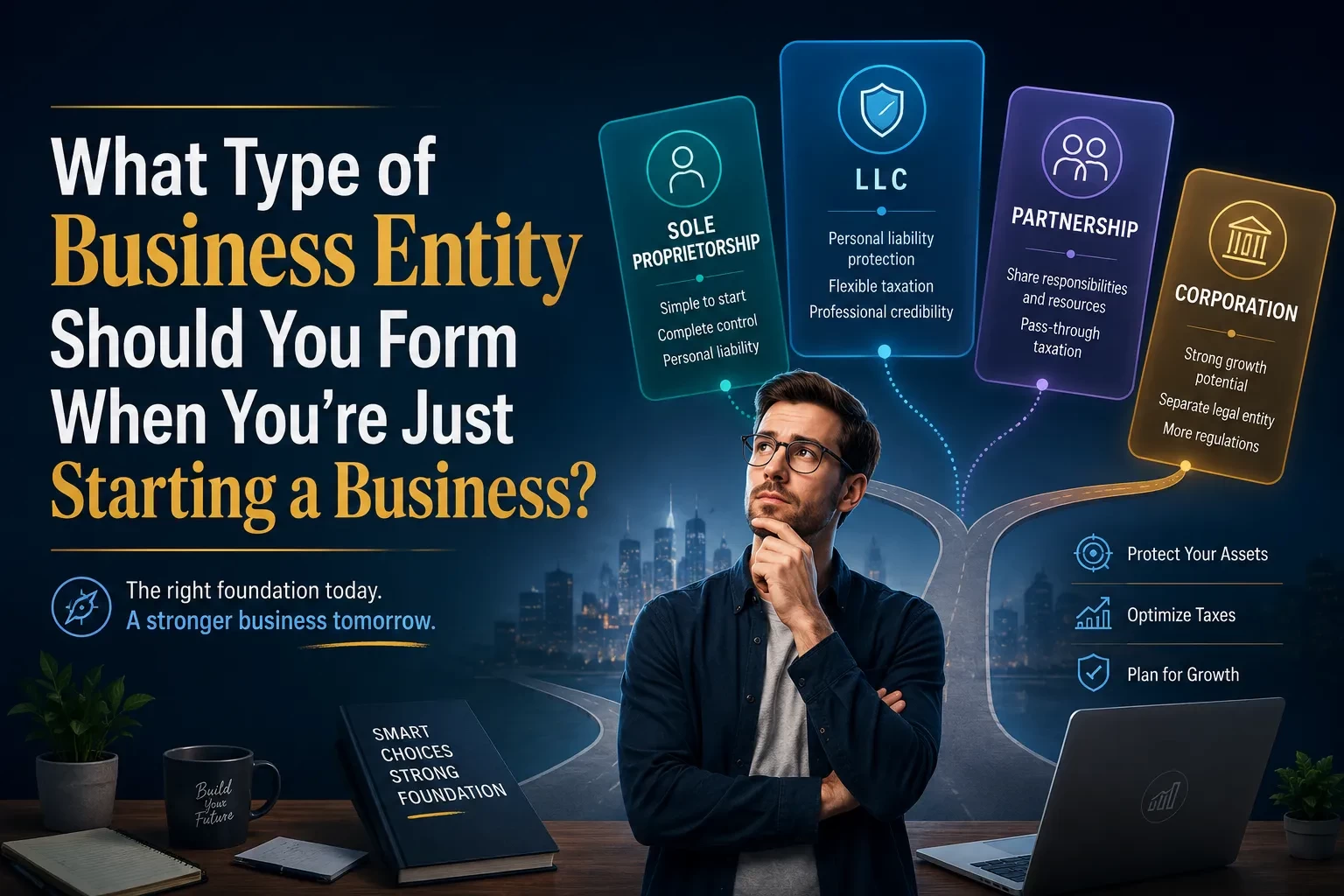

Choosing a business entity is one of the first decisions that makes your business feel “real.” It affects how you pay taxes, how much personal risk you take on, how investors may view you, how much paperwork you manage, and how easily you can open a business bank account or sign contracts. For many first-time founders, freelancers, creators, consultants, ecommerce sellers, and local service providers, the decision usually comes down to a few practical options: sole proprietorship, limited liability company, corporation, or partnership.

This guide is written for U.S. entrepreneurs who are early in the process and want a clear, practical way to choose. We’ll use LegalZoom as the featured business formation platform, but the goal is not to tell you that one structure is right for everyone. Instead, you’ll learn how each entity works, when an LLC makes sense, when a simpler structure may be enough, when a corporation is worth considering, and how to avoid common formation mistakes.

Ready to make your business official with LegalZoom?

Start your business formation process step by step and compare the entity options that fit your goals.

Start with LegalZoomThis is educational information, not legal or tax advice. Before making a final decision, consider speaking with a qualified attorney or tax professional.

Reader Roadmap

• Start with the practical answer: The most common beginner-friendly choice is often an LLC, but not always.

• Understand the entity types: You’ll learn how sole proprietorships, LLCs, corporations, partnerships, and nonprofits differ.

• Use a decision framework: We’ll break the choice down by liability, taxes, ownership, funding plans, and admin workload.

• See where LegalZoom fits: You’ll understand what a formation platform can help with and where professional advice may still be needed.

• Avoid beginner mistakes: We’ll cover common errors around taxes, bank accounts, naming, compliance, and liability protection.

• Leave with next steps: You’ll get a practical checklist for choosing and forming your entity.

The Short Answer: Most New Small Businesses Should Consider an LLC First

For many people just starting a business in the U.S., a limited liability company, or LLC, is the first structure worth evaluating. An LLC is created under state law and is designed to separate the business from the owner personally. The IRS describes an LLC as a business structure allowed by state statute, while also noting that legal and tax considerations matter when selecting a structure (IRS, 2025). (irs.gov)

That matters because a new business often begins informally. You sell a service, test an idea, take your first client, launch a Shopify store, or begin consulting after work. At that stage, you may not feel like you need a “company.” But once customers, contracts, liability risk, business expenses, or revenue enter the picture, entity choice becomes more important.

For a solo founder or small team, an LLC can offer a useful middle ground: more formal than a sole proprietorship, generally simpler than a corporation, and flexible for tax treatment. LegalZoom’s own business formation resources position LLCs as a common option for entrepreneurs who want liability protection and operational flexibility, with LLC formation available through its platform starting at $0 plus state filing fees according to its current LLC overview page (LegalZoom, 2026). (legalzoom.com)

Still, “form an LLC” should not be an automatic answer. A sole proprietorship may be enough if you are testing a very low-risk idea with minimal revenue. A corporation may be better if you plan to raise venture capital. A partnership structure may apply if two or more people are starting together, though it requires extra care. A nonprofit may be appropriate only if your organization is built for a public or charitable purpose, not simply because you want to “do good.”

The decision tree above would help readers visualize the basic path: start with risk and ownership, then move to taxes, funding, and compliance. This matters because choosing an entity is not just a paperwork task; it is a business design decision.

What a Business Entity Actually Does

A business entity is the legal structure through which your business operates. The U.S. Small Business Administration explains that your structure affects day-to-day operations, taxes, and how much of your personal assets are at risk (SBA, 2025). (sba.gov)

In plain English, your entity can affect:

• Liability: Whether your personal assets may be exposed if the business is sued or owes money.

• Taxes: How profits are reported and whether the business pays tax separately from the owner.

• Ownership: Whether you operate alone, with partners, with members, or with shareholders.

• Funding: Whether investors can easily buy ownership in the company.

• Administration: How much paperwork, recordkeeping, and state compliance you must handle.

• Credibility: Whether customers, vendors, lenders, and platforms see you as a more formal operation.

The right structure depends less on what sounds impressive and more on what kind of business you are building.

Form the right business entity with more confidence

LegalZoom can help new founders start an LLC, corporation, nonprofit, or other business structure while keeping the formation process easier to follow.

Explore LegalZoom Business FormationThe Main Business Entity Options for New Founders

Sole Proprietorship: Simple, Fast, but Personally Risky

A sole proprietorship is the default structure for one person doing business without forming a separate legal entity. If you start freelancing under your own name and do not create an LLC or corporation, you are likely operating as a sole proprietor.

The advantage is simplicity. There is usually no separate state formation filing required to become a sole proprietor, though you may still need local licenses, permits, tax registrations, or a “doing business as” name depending on your state and city. You can often start quickly and report business income on your personal tax return.

The tradeoff is liability. A sole proprietorship does not create a separate legal shield between you and the business. If the business is sued, defaults on an obligation, or creates a legal problem, your personal finances may be exposed.

A sole proprietorship can make sense when:

• You are testing an idea before committing money.

• The business has very low liability risk.

• You have no employees.

• You are not signing major contracts.

• Your revenue is small and experimental.

It becomes less attractive when you have paying customers, meaningful revenue, physical products, professional services risk, employees, a lease, business debt, or co-founders.

LLC: The Flexible Default for Many Small Businesses

An LLC is often the practical starting point for new entrepreneurs who want personal liability protection without the heavier structure of a corporation. It can work for consultants, creators, agencies, ecommerce brands, local service businesses, real estate ventures, and many solo-owned companies.

An LLC is not automatically a tax category by itself. For federal tax purposes, the IRS may treat an LLC differently depending on the number of owners and elections made. A single-member LLC is commonly treated as disregarded from its owner by default, while a multi-member LLC is commonly treated as a partnership by default, unless an election is made. LLCs may also elect corporate tax treatment in certain cases (IRS, 2025). (irs.gov)

The practical benefits include:

• Liability separation: The business can be legally distinct from you personally.

• Flexible management: You can usually run the business yourself or define roles in an operating agreement.

• Tax flexibility: Depending on your situation, you may have options beyond the default tax treatment.

• Credibility: Some clients, banks, and vendors prefer working with a registered entity.

• Scalability for small business: An LLC can support growth without immediately requiring corporate formalities.

The limitations include:

• You still need to maintain separation between personal and business finances.

• You may owe state filing fees, annual reports, franchise taxes, or publication costs depending on your state.

• Liability protection is not absolute.

• Some investors prefer corporations, especially Delaware C corporations.

• Tax optimization can become complex as profits grow.

For many beginners, an LLC is not “perfect,” but it is often a strong balance of protection, simplicity, and flexibility.

Corporation: Best for High-Growth, Investor-Oriented Companies

A corporation is a separate legal entity owned by shareholders. It can issue stock, appoint directors, adopt bylaws, and raise capital in ways that are familiar to institutional investors.

There are two common tax-related labels people hear: C corporation and S corporation. A C corporation is taxed separately from its owners. An S corporation is a corporation or eligible entity that elects pass-through tax treatment if it meets IRS requirements. The IRS explains that S corporations pass corporate income, losses, deductions, and credits through to shareholders for federal tax purposes, subject to eligibility rules (IRS, 2025). (irs.gov)

A corporation may make sense when:

• You plan to raise venture capital.

• You want to issue stock options.

• You expect multiple shareholders.

• You are building a high-growth startup.

• You need a structure familiar to sophisticated investors.

• You are comfortable with more governance and compliance.

The downside is complexity. Corporations involve more formalities, including bylaws, board meetings, shareholder records, stock issuance, and potentially more tax complexity. For a solo consultant, local service provider, or early ecommerce seller, that may be unnecessary at the beginning.

Partnership: Useful for Co-Founders, Risky Without Agreements

A partnership generally involves two or more people carrying on a business together. Like sole proprietorships, some partnerships can arise by default if people begin operating together without forming another entity.

The key issue is that partnerships can create shared liability and decision-making problems if the founders do not document expectations. Who owns what percentage? Who contributes money? Who owns the brand? Who can sign contracts? What happens if one person wants to leave?

A partnership may be appropriate when:

• Two or more people are starting together.

• The business is still early and informal.

• Everyone understands the risks.

• A written partnership agreement is in place.

Many co-founders instead choose to form a multi-member LLC because it can provide a more structured operating agreement and potential liability protection.

Nonprofit: Only for a Public or Charitable Mission

A nonprofit is not simply a business that has not made money yet. It is a structure designed for organizations serving a public, charitable, educational, religious, scientific, or similar purpose. LegalZoom lists nonprofit formation as one of its business formation categories, and its page describes a nonprofit as a structure designed to support a public or social benefit that can be eligible for tax breaks (LegalZoom, 2026). (legalzoom.com)

A nonprofit may make sense if your mission, funding, governance, and operations fit nonprofit rules. It is usually not the right choice for a standard for-profit startup, agency, shop, app, or consulting business.

Entity Comparison for First-Time Founders

| Entity type | Best for | Main advantage | Main drawback |

|---|---|---|---|

| Sole proprietorship | Testing a low-risk solo idea | Simple and inexpensive to start | No personal liability separation |

| LLC | Most solo founders and small businesses wanting flexibility | Liability separation with manageable complexity | Ongoing state compliance and fees |

| Corporation | Startups raising capital or issuing stock | Investor-friendly structure | More governance, paperwork, and tax complexity |

| Partnership | Two or more people starting together informally | Simple shared ownership | Risky without a strong written agreement |

| Nonprofit | Public-benefit or charitable missions | Mission-driven structure with possible tax benefits | Strict governance and eligibility requirements |

This comparison is intentionally simple. Your state, industry, tax situation, and risk profile can change the answer.

How LegalZoom Fits Into the Business Formation Decision

LegalZoom is an online legal technology platform that helps users form business entities such as LLCs, corporations, nonprofits, DBAs, and related filings. Its business formation page says the company has supported more than 4 million formations and has more than 25 years of experience (LegalZoom, 2026). (legalzoom.com)

For a new founder, the value of a platform like LegalZoom is usually in workflow and convenience. Instead of hunting through state filing pages, trying to understand required documents, and worrying about missed steps, you can use a guided process that asks for your business name, state, ownership details, management structure, and related services.

LegalZoom may help with:

• Choosing from common entity types.

• Preparing and filing formation documents.

• Checking name availability in the formation workflow.

• Creating basic legal documents.

• Obtaining an EIN in some service packages or workflows.

• Accessing registered agent services.

• Building a compliance calendar or ongoing filing support.

• Filing a DBA if you want to operate under a brand name.

However, LegalZoom should not be treated as a substitute for personalized legal or tax advice when your situation is complex. If you have co-founders, investors, intellectual property, regulated services, employees, significant liability risk, or multi-state operations, professional advice can prevent expensive mistakes.

The Practical Decision Framework: How to Choose Your Entity

Instead of asking, “Which entity is best?” ask a better question: “Which entity fits my current risk, tax needs, ownership plan, and growth path?”

1. Start With Liability Risk

Liability means the possibility that the business could owe money, be sued, damage property, cause financial harm, or create legal obligations.

Higher-risk businesses include:

• Physical products.

• Food, health, wellness, or childcare services.

• Construction, repair, or home services.

• Professional advice or consulting with financial consequences.

• Businesses with employees or contractors.

• Businesses that use vehicles, equipment, or customer property.

• Businesses signing larger contracts.

If your business has meaningful liability exposure, a sole proprietorship may be too thin. An LLC or corporation is usually worth evaluating.

2. Look at Ownership

If you are the only owner, the decision is simpler. You may compare sole proprietorship, single-member LLC, and corporation.

If you have co-founders, do not rely on verbal agreements. You need a structure that defines ownership, responsibilities, voting, exits, profit distribution, and dispute resolution. A multi-member LLC with an operating agreement may work for many small businesses. A corporation may be better if you plan to issue shares, raise outside capital, or create equity incentives.

3. Consider Taxes, but Don’t Start With Taxes Alone

Tax treatment matters, but it should not be the only driver. A structure that saves a little on taxes but exposes you to personal liability or investor problems may not be worth it.

For example, some owners explore S corporation taxation once their business is profitable enough to justify payroll, accounting, and compliance costs. But S corporation status has rules and limitations. The IRS has specific requirements for S corporations, including limits on shareholder type and number (IRS, 2025). (irs.gov)

Early-stage founders should usually ask:

• How will income be reported?

• Will I need payroll?

• Will I owe self-employment tax?

• Does my state impose franchise or annual taxes?

• Will my bookkeeping support the structure I choose?

A CPA can often save you more money than guessing.

4. Think About Funding

If you plan to bootstrap, freelance, sell services, operate locally, or build a lifestyle business, an LLC may be enough.

If you plan to raise venture capital, apply to accelerators, issue stock options, or build toward acquisition, a corporation may be more appropriate. Many venture-backed startups use Delaware C corporations because investors are familiar with that structure. That does not mean every business should copy venture-backed startups.

5. Evaluate Administrative Burden

A simple structure is easier to maintain. But too simple can create risk. The right choice should match your willingness and ability to handle compliance.

Ask:

• Do I need annual state reports?

• Do I need a registered agent?

• Do I need meeting minutes or bylaws?

• Do I need an operating agreement?

• Do I need separate tax filings?

• Do I need licenses or permits?

• Do I need bookkeeping software?

LegalZoom and similar platforms can help organize the formation process, but you still need to maintain the business after formation.

The workflow diagram above would show why formation is only one stage. A new entity still needs tax setup, banking, records, licenses, and ongoing compliance.

Step-by-Step: How to Choose and Form Your First Business Entity

1. Define the Business You Are Actually Starting

Before choosing an entity, write a one-paragraph description of the business.

Include:

• What you sell.

• Who pays you.

• Whether you provide services, products, software, content, or physical work.

• Whether you operate online, locally, or across states.

• Whether you have co-founders.

• Whether you plan to hire.

• Whether the business has safety, financial, or legal risk.

This prevents you from choosing an entity based on vague startup advice.

2. Decide Whether You Need Liability Protection Now

If you are only brainstorming, researching, or validating with no sales, you may not need to form immediately.

If you are taking payments, signing contracts, collecting customer data, selling products, entering homes, giving advice, renting space, or hiring help, liability separation becomes more important.

An LLC is often the first structure to evaluate at this stage because it can create a legal separation between you and the business while remaining manageable for small operators.

3. Compare LLC vs. Corporation Based on Growth Plans

Choose an LLC if:

• You want a flexible small business structure.

• You are bootstrapping.

• You do not need to issue stock.

• You want simpler management.

• You want liability separation without corporate formalities.

Consider a corporation if:

• You plan to raise venture capital.

• You need stock options.

• You expect multiple shareholders.

• You are building a scalable tech startup.

• Your investors or accelerator require it.

A corporation can be powerful, but it is often more structure than a beginner needs.

4. Choose Your Formation State

For most small businesses, forming in your home state is often simpler because that is where you operate, pay taxes, maintain licenses, and may need to register anyway.

Some founders hear that they should form in Delaware, Nevada, or Wyoming. That may be useful in specific cases, especially investor-backed companies. But if you live and operate in another state, forming elsewhere may create extra foreign qualification, registered agent, and compliance costs.

Ask:

• Where do I physically operate?

• Where are my customers?

• Where do I have employees or contractors?

• Where do I need licenses?

• Will forming out of state create duplicate fees?

5. Check Business Name Availability

Your name needs to work legally, practically, and commercially.

Check:

• State business name availability.

• Trademark conflicts.

• Domain name availability.

• Social media handles.

• Whether the name is easy to spell.

• Whether it limits future growth.

A state name approval does not automatically mean you have trademark rights. If the brand matters, consider a trademark search and legal review.

6. Prepare Formation Documents

For an LLC, this typically means filing articles of organization or a certificate of formation with the state. For a corporation, it usually means filing articles of incorporation or a certificate of incorporation.

A platform like LegalZoom can guide you through the information needed for the filing, such as business name, state, registered agent, business address, and ownership details. LegalZoom’s business formation page organizes common formation options including LLCs, corporations, nonprofits, DBAs, and partnerships (LegalZoom, 2026). (legalzoom.com)

7. Create Internal Documents

Do not stop after the state filing.

For an LLC, create an operating agreement. Even single-member LLCs benefit from one because it documents how the company is managed and reinforces separation between owner and business.

For a corporation, create bylaws, appoint directors, authorize shares, issue stock properly, and maintain corporate records.

For partnerships, create a written partnership agreement before money comes in.

8. Get an EIN

An Employer Identification Number, or EIN, is a federal tax identification number issued by the IRS. Many businesses need one to open a bank account, hire employees, or file certain tax returns. You can apply directly through the IRS, and the IRS provides online tools for business tax responsibilities (IRS, 2025). (irs.gov)

9. Open a Business Bank Account

Liability protection depends partly on acting like the business is separate from you. Mixing personal and business money can weaken that separation.

Set up:

• A business checking account.

• A bookkeeping system.

• A payment processor account.

• A dedicated business credit card if appropriate.

• A recordkeeping process for receipts and invoices.

10. Build a Compliance Calendar

Your business may need annual reports, franchise tax filings, registered agent renewals, business licenses, sales tax filings, payroll filings, and insurance renewals.

FinCEN’s beneficial ownership information rules have changed significantly. As of FinCEN’s March 2025 interim final rule, U.S.-created entities and U.S. persons were exempted from BOI reporting requirements, while certain foreign companies remained subject to reporting rules (FinCEN, 2025). (fincen.gov) Because these rules have shifted, founders should verify current requirements before relying on old checklists.

Practical Examples: Which Entity Fits Which Beginner?

Example 1: Freelance Designer With First Clients

You design websites and branding assets for small businesses. You work from home, have no employees, and expect $25,000 to $60,000 in first-year revenue.

A sole proprietorship may work at the earliest testing stage. But once contracts and client deliverables become consistent, an LLC is worth considering for liability separation and professionalism. You should also use written contracts, business insurance, and a separate bank account.

Example 2: Two Friends Launching a SaaS Tool

You and a co-founder are building a software product. You may apply to accelerators and raise money within 12 months.

A corporation may be worth discussing with a startup attorney early, especially if equity, vesting, intellectual property assignment, and fundraising are part of the plan. An LLC can work for some software businesses, but venture investors often prefer corporations.

Example 3: Local Cleaning Business

You plan to clean homes and offices, hire contractors, and use equipment at customer locations.

An LLC is likely more appropriate than a sole proprietorship because there is customer property risk, contractor risk, and operational liability. You may also need insurance, local permits, and strong service agreements.

Example 4: Educational Community Project

You want to run free community workshops funded by donations and grants.

A nonprofit may be appropriate if the project has a public-benefit mission and will operate under nonprofit governance rules. This is not the same as forming a normal small business. You may need nonprofit formation, tax-exempt application support, and board governance documents.

Cost and ROI Considerations

Entity formation costs vary by state, structure, and service level. Some costs are obvious, such as state filing fees. Others appear later, such as annual reports, registered agent renewals, publication requirements, franchise taxes, CPA fees, payroll costs, and legal document updates.

LegalZoom’s LLC formation page currently advertises LLC formation starting at $0 plus state filing fees, but optional services, state costs, registered agent services, tax help, operating agreements, and compliance support can increase the total cost (LegalZoom, 2026). (legalzoom.com)

The return on forming an entity is not just tax savings. It can include:

• Lower personal risk.

• Easier banking.

• More professional contracts.

• Cleaner accounting.

• Better co-founder documentation.

• Better preparation for hiring.

• Stronger credibility with vendors and clients.

However, forming too early can also create unnecessary fees if the idea never launches. The right timing is usually when you move from “experiment” to “business activity.”

When Not to Form an LLC Yet

An LLC is useful, but not every idea needs one immediately.

You may wait if:

• You are still researching.

• You have no revenue.

• You have not chosen a business model.

• You are not signing contracts.

• You are not taking customer payments.

• You are not exposing yourself to meaningful liability.

• You are still deciding whether to continue.

Waiting does not mean ignoring risk. It means matching structure to reality. You can validate demand first, then form when the business becomes active.

Common Mistakes and Troubleshooting

mistake 1: Thinking an LLC Protects You From Everything

An LLC can help separate business liability from personal assets, but it does not protect against every risk. You can still be liable for personal wrongdoing, fraud, unpaid taxes, personal guarantees, or sloppy separation between business and personal finances.

Fix: Keep separate accounts, sign contracts in the company’s name, avoid personal guarantees when possible, maintain insurance, and follow state compliance rules.

Mistake 2: Mixing Personal and Business Money

Many founders form an LLC but keep using a personal checking account. That undermines clean accounting and can create problems during tax season or disputes.

Fix: Open a business bank account as soon as your entity is formed and your EIN is available. Route income and expenses through the business account.

Mistake 3: Choosing a Corporation Because It Sounds More Serious

A corporation can be the right structure for investor-backed companies, but it may be unnecessary for a small service business.

Fix: Choose based on funding plans, ownership needs, and compliance capacity—not prestige.

Mistake 4: Ignoring State-Specific Rules

Entity rules vary by state. Fees, reports, taxes, publication requirements, and naming rules can differ widely.

Fix: Check your Secretary of State website and state tax agency. If you use LegalZoom or another service, still read the state-specific requirements you receive.

Mistake 5: Forgetting Licenses and Permits

Forming an LLC does not automatically give you permission to operate. Some businesses need local licenses, sales tax permits, professional licenses, health permits, or zoning approval.

Fix: Search requirements by city, county, state, and industry before launching publicly.

Mistake 6: Not Having a Co-Founder Agreement

Two friends can start with trust and still end in conflict when money, workload, or ownership expectations differ.

Fix: Use an operating agreement, partnership agreement, stock agreement, vesting terms, and IP assignment documents where appropriate. Get legal help before revenue or investment arrives.

Mistake 7: Relying on Old Compliance Advice

Business compliance changes. The BOI reporting rules are a good example: requirements shifted through litigation, agency announcements, and interim rule changes in 2025 (FinCEN, 2025). (fincen.gov)

Fix: Verify current requirements with official sources, not old blog posts or outdated social media threads.

The checklist above would work well as a visual summary of the biggest post-formation risks. It reminds readers that the entity filing is the beginning of compliance, not the end.

LegalZoom vs. DIY vs. Hiring an Attorney

LegalZoom is useful when you want a guided, structured formation process and do not want to navigate every filing step manually. DIY formation may be cheaper if you are comfortable with state forms and know exactly what you need. Hiring an attorney is more expensive but can be worth it when the stakes are higher.

Use LegalZoom When:

• You want a guided formation process.

• Your structure is relatively standard.

• You want help organizing documents and filings.

• You value convenience over doing everything manually.

• You may need related services like registered agent support, DBA filing, or legal document templates.

Go DIY When:

• Your business is very simple.

• You understand your state’s filing requirements.

• You are comfortable reading government instructions.

• You want the lowest possible filing cost.

• You do not need customized advice.

Hire an Attorney When:

• You have co-founders.

• You are raising money.

• You are issuing equity.

• You have valuable intellectual property.

• You operate in a regulated industry.

• You are signing high-value contracts.

• You have multi-state or international complexity.

A smart approach is not “LegalZoom or lawyer.” Many founders use a platform for straightforward formation and then consult an attorney or CPA for specific issues.

Privacy, Compliance, and Data Considerations

When forming a business online, you will provide personal and business information. That may include your name, address, ownership details, payment information, and business contact details.

Before using any formation platform, review:

• What information becomes part of public state records.

• Whether you need a registered agent address for privacy.

• How your data is stored and used.

• Whether optional services renew automatically.

• What documents you can download and keep.

• What deadlines remain your responsibility.

A registered agent service may help keep your personal address off some public-facing records, depending on your state and filing type. But privacy is not absolute. State business records, tax registrations, licenses, and court filings may still reveal information.

The Beginner’s Entity Selection Checklist

Before you form anything, answer these questions:

• Am I earning revenue or still testing?

• What could go wrong if a customer, vendor, or partner complains?

• Do I have co-founders?

• Will I hire employees or contractors?

• Will I raise outside investment?

• Do I need to issue equity?

• Do I sell physical products?

• Do I provide professional advice?

• What state do I operate in?

• What licenses or permits do I need?

• Can I keep business and personal finances separate?

• Do I have a CPA or tax plan?

• Do I need an attorney to review ownership or contracts?

If most answers point to real customers, real risk, and real operations, forming an LLC or corporation is likely worth serious consideration.

FAQ

Conclusion: Choose the Entity That Matches Your Risk and Growth Plan

If you are just starting a business, the best entity is the one that matches your actual stage, risk, ownership, and goals. For many U.S. small business owners, an LLC is the most practical first structure because it offers liability separation, flexibility, and manageable administration. But it is not universal. A sole proprietorship may be fine for early testing. A corporation may be better for venture-backed startups. A partnership needs careful agreements. A nonprofit belongs to mission-driven public-benefit work, not ordinary for-profit businesses.

LegalZoom can be a useful formation tool if you want a guided process and a faster path from idea to registered entity. Use it as part of a broader setup: choose the right structure, understand your state requirements, create internal documents, get an EIN, open a business bank account, track compliance, and get tax or legal advice where needed.

Your quick next-step checklist:

• Define the business model in one paragraph.

• Identify your liability risk.

• Decide whether you have co-founders or investors.

• Compare sole proprietorship, LLC, and corporation.

• Check your state’s fees and annual requirements.

• Choose a business name and verify availability.

• Form the entity through your state, LegalZoom, or an attorney.

• Create internal documents.

• Get an EIN if needed.

• Open a business bank account.

• Build a compliance calendar.

• Talk to a CPA before tax season.

Sources

• LegalZoom — Business Formation — https://www.legalzoom.com/business/business-formation/

• LegalZoom — Start an LLC — https://www.legalzoom.com/business/business-formation/llc-overview.html

• LegalZoom — How to Start an LLC in 7 Steps — https://www.legalzoom.com/articles/how-to-start-an-llc-in-7-steps

• U.S. Small Business Administration — Choose a Business Structure — https://www.sba.gov/business-guide/launch-your-business/choose-business-structure

• Internal Revenue Service — Business Structures — https://www.irs.gov/businesses/small-businesses-self-employed/business-structures

• Internal Revenue Service — Main IRS Business Tax Resources — https://www.irs.gov/

• FinCEN — Beneficial Ownership Information Reporting — https://www.fincen.gov/boi

• FinCEN — BOI Reporting Requirements Update for U.S. Companies and U.S. Persons — https://www.fincen.gov/news/news-releases/fincen-removes-beneficial-ownership-reporting-requirements-us-companies-and-us

Start Your Business Formation with LegalZoom